Micro Insurance Market Overview:

The global micro insurance market, a vital financial instrument for low-income individuals and underserved communities, is experiencing rapid growth. In 2022, the market was valued at USD 49.29 billion and is projected to grow from USD 54.52 billion in 2023 to USD 135.4 billion by 2032. This reflects a compound annual growth rate (CAGR) of 10.63% during the forecast period from 2024 to 2032. The rise in demand for affordable insurance solutions among the world’s most vulnerable populations is driving this market expansion.

Understanding Micro Insurance

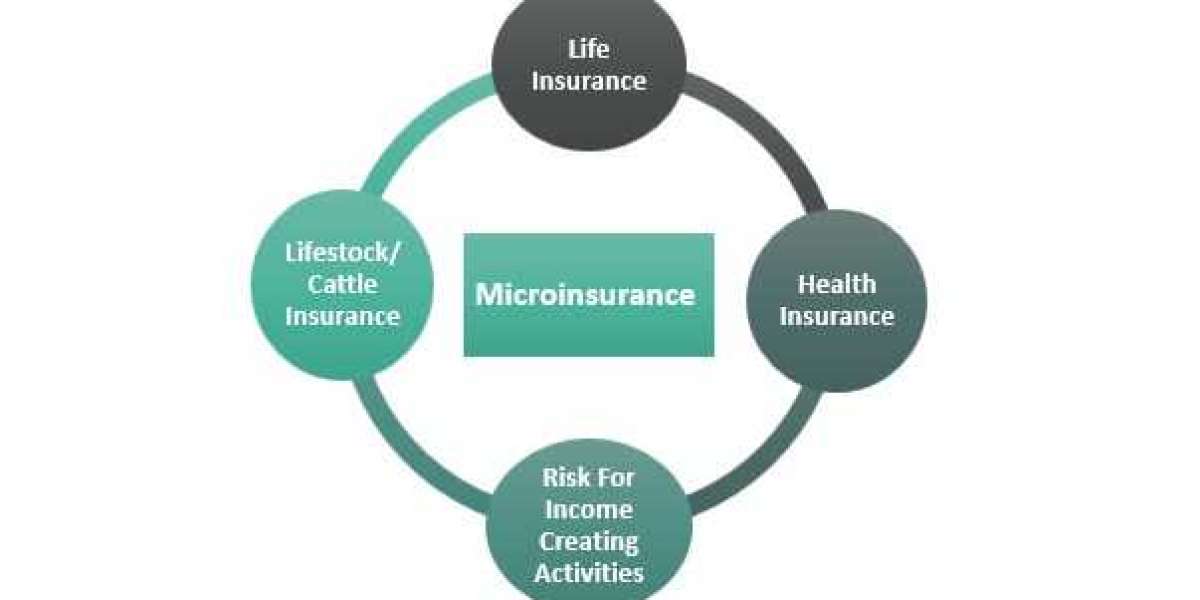

Micro insurance is a type of insurance designed to provide financial protection to individuals with low incomes, particularly in developing and emerging economies. These products typically offer coverage for health, life, property, agriculture, and small businesses, tailored to meet the specific risks and financial limitations of the insured. Unlike conventional insurance, micro insurance policies often have lower premiums, simplified terms, and accessible claims processes to accommodate the needs of low-income policyholders.

Request For Sample Report PDF - https://www.marketresearchfuture.com/sample_request/24664

Key Market Drivers

Several factors are contributing to the robust growth of the micro insurance market:

Rising Demand in Emerging Economies: As economic development progresses in emerging markets, more people are seeking financial security through insurance products. Micro insurance serves a growing segment of the population that was previously underserved by traditional insurance providers.

Government Initiatives and Support: Governments, particularly in developing countries, are recognizing the importance of financial inclusion and are promoting micro insurance as a tool to alleviate poverty and support economic resilience. Some governments have introduced policies that encourage or mandate micro insurance coverage for vulnerable populations.

Technological Advancements: The proliferation of digital platforms, mobile banking, and fintech solutions has made micro insurance more accessible to low-income individuals. Mobile insurance platforms, in particular, are revolutionizing the way policies are distributed and claims are processed, significantly improving market penetration in remote areas.

Rising Awareness of Risk Management: As awareness of the importance of risk management grows, more low-income individuals are seeking insurance to safeguard themselves against unforeseen events such as health issues, natural disasters, or loss of income.

Partnerships with NGOs and Microfinance Institutions: Collaborations between insurance providers, non-governmental organizations (NGOs), and microfinance institutions (MFIs) have expanded the reach of micro insurance products. These partnerships enable insurers to leverage existing networks and relationships with underserved communities, ensuring wider adoption of micro insurance policies.

Challenges in the Micro Insurance Market

Despite its promising growth prospects, the micro insurance market faces several challenges:

Limited Awareness and Education: In many regions, potential customers are unaware of the benefits of micro insurance or do not fully understand how it works. This lack of awareness, coupled with low financial literacy, poses a significant barrier to market growth.

Low Profit Margins for Insurers: The relatively low premiums associated with micro insurance policies can make it challenging for insurers to achieve profitability. As a result, some traditional insurance companies may be hesitant to invest in this segment of the market.

Regulatory Challenges: Varying regulatory environments across countries can make it difficult for insurance companies to operate consistently in the micro insurance space. Regulatory barriers can also complicate product design and distribution.

Distribution and Infrastructure Constraints: In many developing regions, the lack of physical infrastructure, such as banks or insurance offices, makes it difficult to reach potential customers. Insurers must rely on innovative distribution methods, such as mobile platforms, to overcome these barriers.

Market Segmentation

The micro insurance market can be segmented based on the type of coverage and the target population.

By Coverage Type

Life Insurance: Micro life insurance provides coverage for death or disability, offering financial support to beneficiaries and helping families manage the economic impact of losing a breadwinner.

Health Insurance: Health micro insurance is designed to cover basic medical expenses, offering protection against the financial burden of illness or injury. It is particularly valuable in regions where healthcare costs are high relative to income levels.

Agriculture Insurance: Agricultural micro insurance provides protection to farmers against risks such as crop failure, livestock loss, or adverse weather conditions. This type of insurance is crucial in rural areas where agriculture is the primary source of livelihood.

Property Insurance: Micro property insurance covers damage or loss of personal property, such as homes, equipment, or livestock, due to natural disasters, accidents, or theft.

By Target Population

Rural Populations: In many developing countries, rural populations are highly vulnerable to natural disasters, crop failures, and health crises. Micro insurance provides these communities with essential financial protection.

Urban Low-Income Groups: Micro insurance is increasingly being offered to low-income workers in urban areas, providing coverage for healthcare, life insurance, and property protection.

Women and Marginalized Communities: Micro insurance providers are increasingly focusing on women and marginalized groups, who are often excluded from formal financial services. Tailored products can address the specific risks these groups face, such as health risks or the loss of a primary caregiver.

Regional Insights

Asia-Pacific: The Asia-Pacific region is expected to lead the global micro insurance market in terms of growth. Countries like India, China, and Indonesia have large low-income populations and are witnessing strong government support for micro insurance initiatives. Mobile insurance platforms are also gaining traction in this region, further driving market growth.

Africa: Africa presents significant opportunities for the micro insurance market, particularly in regions where large portions of the population rely on agriculture for their livelihoods. Countries like Kenya, Nigeria, and South Africa have seen increased adoption of micro insurance products, thanks to partnerships between insurers, NGOs, and microfinance institutions.

Latin America: In Latin America, countries such as Brazil, Mexico, and Colombia are emerging as key markets for micro insurance. The region has seen growing efforts to extend financial services to underserved populations, and micro insurance is a central part of this push for financial inclusion.

Middle East: While still a developing market, the Middle East is seeing increased interest in micro insurance as part of broader financial inclusion initiatives. Governments in the region are recognizing the need to provide low-income individuals with access to insurance products.

Future Outlook

The micro insurance market is set for significant expansion over the coming decade, with a projected market size of USD 135.4 billion by 2032. Key drivers of this growth include technological advancements, government support, and rising awareness of the benefits of insurance in low-income populations. As the market evolves, insurers are expected to offer more innovative and affordable products tailored to the unique needs of underserved communities.

Additionally, the growth of mobile and digital platforms will continue to improve accessibility and ease of use, further enhancing the market's reach. Partnerships between insurance providers, microfinance institutions, and non-governmental organizations will also be critical in extending micro insurance coverage to hard-to-reach areas.

Conclusion

The global micro insurance market is poised for robust growth, driven by increasing demand for affordable insurance products among low-income populations in emerging markets. As the industry addresses challenges such as financial literacy and regulatory barriers, it will continue to play a crucial role in fostering financial inclusion and economic resilience. By 2032, the market is expected to more than double in size, reflecting the growing importance of micro insurance as a tool for risk management and poverty alleviation.